Unit: 4 Materials Management and Inventory Control (Theory)

Syllabus

- 4.1 Objectives & Functions of materials Management

- 4.2 Purchase procedure – steps involved in purchasing

- 4.3 Stores Management – Functions, BIN card

- 4.4 Objectives of Inventory control, Maximum & Minimum Stock, Lead Time, Reorder Level- Economic Order Quantity, ABC analysis and VED analysis of Inventory, Break Even analysis

4.1 Objectives & Functions of Materials Management

Material Management

Materials Management is the planning, directing, controlling and coordinating those activities which are concerned with materials and inventory requirements, from the point of their introduction into the manufacturing process.

Note:

Thus, material management is an important function of an organisation covering various aspects of input process, i.e., it deals with raw materials, procurement of machines and other equipment’s necessary for the production process and spare parts for the maintenance of the plant. Thus, in a production process materials management can be considered as an preliminary to transformation process.

Components of Material Management

- Purchase & Contract Management

- Supply Chain & Logistics Management

- Stores Management

- Inventory Management

- Supplier Relationship Management

Activities Involved in Material Management

- Material Requirement Planning (MRP)

- Purchasing

- Inventory Control

- Expediting

- Transportation

- Material Handling

Functions of Materials Management

- Materials Planning: It involves forecasting demand and quantity of materials required, preparing materials budget, forecasting the levels of inventories and scheduling the orders.

- Purchasing: It involves choosing right sources of material supply, placing of purchase orders, follow-up, keeping good relations with suppliers, payments to suppliers and evaluating suppliers.

- Procurement: Procurement of materials, transportation, quality control and inspection of purchased materials and components.

- Stores Management: It includes conservation of materials in stores, efficient handling, maintaining stores records, proper location and stocking, scrap, surplus and obsolete materials disposal.

- Inventory Control: Efficient inventory control is a must to ensure timely availability of material at minimum cost.

- Preparing Standardization, Simplification and Specifications of materials.

- Value analysis of costly materials.

- Ensuring smooth flow of materials in and out of the organization.

- Packaging, warehouse planning, accounting, finished goods safety and care.

Techniques of Material Management

The modern techniques of material management are as follows:

- Just-in-time (JIT)

- System Applications and Products (SAP)

- Enterprise Resource Planning (ERP)

4.2 Purchase procedure – steps involved in purchasing

Purchasing Management

The purchasing can be defined as the process of buying and procuring the materials, parts, components, equipment, spare parts, tools and supporting items required by industries or any organization to deliver its products as per customer requirements at the competitive rates and of good quality.

Note:

Purchasing is an important function of materials management. In any industry purchase means buying of equipment, materials, tools, parts etc. required for industry. The importance of the purchase function varies with nature and size of industry. In small industry, this function is performed by works manager and in large manufacturing concern; this function is done by a separate department.

Steps Involved in Purchasing

The Various Steps Involved in Purchasing

- (a) Determination of Purchase Budget.

- (b) Receiving Purchase Requisition slips.

- (c) Tapping the sources of supply.

- (d) Placing the order.

- (e) Receipt of Materials.

- (f) Checking the Invoices.

Procedures of Purchasing

Whenever a department needs an item, it is officially brought to the notice of the purchasing department, by filling a purchase requisition slip. After receiving the purchase requisition forms, exact quantity of material to be purchased and its specification is decided. Then prepare a list of suppliers who deal with the business of articles to be purchased and are reliable. If material to be purchased is small amount and required urgently, it may be purchased locally. Prepare a comparative statement of the rates, terms and conditions mentioned in the quotations and then analyze them.

4.3 Stores Management

Stores Management

Stores Management deals with undertaking the right type of materials in sufficient quantity, in a prompt manner whenever needed, to keep it safe against any sort of damage, pilferage, or theft.

It is a part of material management. It involves actual material handling which is received held and issued. A store is a place where the material is kept in such a manner that it can be accounted for and safely maintained and it can be used when required.

Functions of Store Management

There are three main functions in which operations at the store level are classified:

- Personnel

- Administration

- Selling

Who is Store Manager?

A store manager is an individual who is charged with the day-to-day operations or management of the retail store. The entire store staff reports to the store manager.

Functions of Store Management

- Maintaining store facilities

- Planning work schedules

- Recruitment and Training of workforce to work in stores.

- Performance evaluation of store staff

- Locating and displaying the merchandise.

- Preventing shrinkage of inventory.

- Physical stock taking

- Assisting customers in the selection

- Handling customer complaints

- Providing services like packaging and home delivery.

- Ensuring accurate inventory.

Bin Card

BIN is the short form of Business Identification Number. It is used in store for inventory control. In a storeroom, materials and other items are kept in appropriate bins, drawers or other receptacles; some items are stacked, while others are racked. For each kind of material, a separate record is kept on a BIN CARD or Stock Card which shows details of the quantity of material received by, issued to and remained in stores. Bin card is attached to each bin or shelf. A bin card is not considered as an accounting record; it simply informs storekeeper of the quantities of each item on hand Bin cards are checked periodically by the store’s inspectors to see that they are accurately maintained.

4.4 Inventory Control

Inventory Management

It is a component of Material Management of an organisation. Inventory is defined as any idle resources of an enterprise. It is a physical stock of goods kept for future use. In a factory, the inventory may be in the form of raw material, parts, semi-finished goods etc. An inventory may also include furniture, machinery etc.

Inventory Management Objectives

Inventory management is performed to simplify the operational activities. Some of the primary objectives for which it is carried out are as follows:

- Preventing Dead Stock or Perishability: The chances of wastage in the form of goods spoilage or dead stock reduces.

- Optimizing Storage Cost: It reduces the chances of maintaining excessive stock, which ultimately cuts down the unnecessary warehousing costs.

- Maintaining Sufficient Stock: The production department need not worry about the shortage of raw material or goods because of its constant supply.

- Enhancing Cash Flow: With effective inventory management, the organization can ensure sufficient liquid cash to enhance its operational efficiency.

- Reducing the Inventory Cost: When there is a constant purchase of goods or stock, the organization can ask for discounts and other benefits to decrease the purchase price.

Types of Inventories

- Raw Material Inventory

- In-process Inventory

- Finished Product Inventory

Raw Material Inventory:

It includes raw material, semi-finished components, standard components /subassemblies purchased from suppliers.

In-process Inventory:

It consists of semi-finished components, subassemblies and products at various stages of the manufacturing cycle. In-process inventory is the term used for all material on the shop floor at various machines or in various departments.

Finished Product Inventory:

It includes the lubricants, cutting fluids, cotton waste, stationery, cutting tools and spare parts needed for proper operation, repair and maintenance.

Techniques of Inventory Management

There are many inventory management techniques available –

- EOQ (economic order quantity),

- ABC analysis,

- Just-in-time Inventory Management,

- EQR model,

- VED analysis,

- LIFO (last in last out)

- FIFO (first in first out).

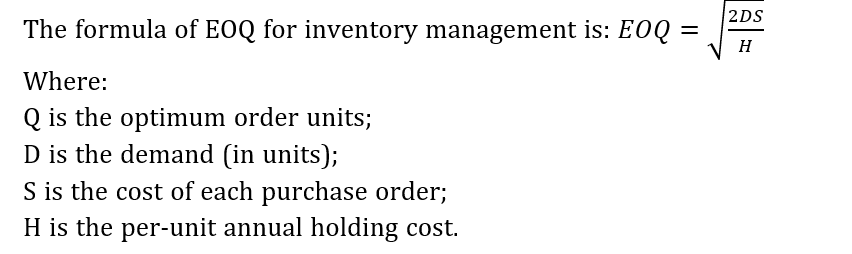

Economic Order Quantity (EOQ)

EOQ is used as an inventory management method to estimate the optimum quantity of material to be purchased, to fulfil the production requirement such that the inventory maintenance cost is minimal.

Inventory Cost

Costs Associated with Inventory Management are

- Purchase Costs (purchase price of the items or raw materials)

- Ordering costs Ordering costs/Set Up Costs/Procurement Cost (Costs associated with the processing and chasing of the purchase order, transportation, quality inspection etc.)

- Carrying cost/Holding Cost (Storage and maintenance etc.)

- Stock out cost or, Shortage cost (cost related to insufficient inventory – unable to meet & satisfy demand)

Economic Order Quantity (EOQ)

ABC Analysis

Another inventory control method is ABC analysis that lists out the goods under three classes as follows:

A – Highly Important: These are the goods which cost high and therefore, maintained in small quantity.

B – Moderately Important: It constitutes the inventory which has an average value maintained in fair quantity.

C – Less Important: These goods are available in huge quantity due to their low value or cost.

VED Analysis /Vital, Essential and Desirable Analysis

The VED classification is mostly used in industries where machines are used for production. It distinguishes the stock according to the significance of its usage into the following three categories:

Vital: Items signifying the lifeline of the production process are termed as vital items. In the absence of these, the whole process would halt.

Essential: The stockout cost of the essential items is quite high. Thus, their absence leads to a significant loss.

Desirable: The desirable items do not immediately hamper the production and also have a minimal stock out the cost.

In the above classification, we can see that the essential items hold the highest significance since its non-availability would pause the production process. These items usually comprise of machinery which requires excessive control.

Break-even Analysis

A break-even analysis is an economic tool that is used to determine the cost structure of a company or the number of units that need to be sold to cover the cost. Break-even is a situation where a company neither makes a profit nor loss but recovers all the money spent. The break-even analysis is used to examine the relation between the fixed cost, variable cost, and revenue. Usually, an organisation with a low fixed cost will have a low break-even point of sale.

Components of Break-even Analysis

Fixed costs: These costs are also known as overhead costs. These costs includes one-time financial activity of a business at its start. The fixed prices include taxes, salaries, rents, depreciation cost, labour cost, interests, energy cost, etc.

Variable costs: These costs fluctuate and will decrease or increase according to the volume of the production. These costs include packaging cost, cost of raw material, fuel, and other materials related to production.

Break Even Formula

——End of Unit 4 Notes——

Previous Year Questions:

2023 July Work Organisation Management Semester 6 Question Paper